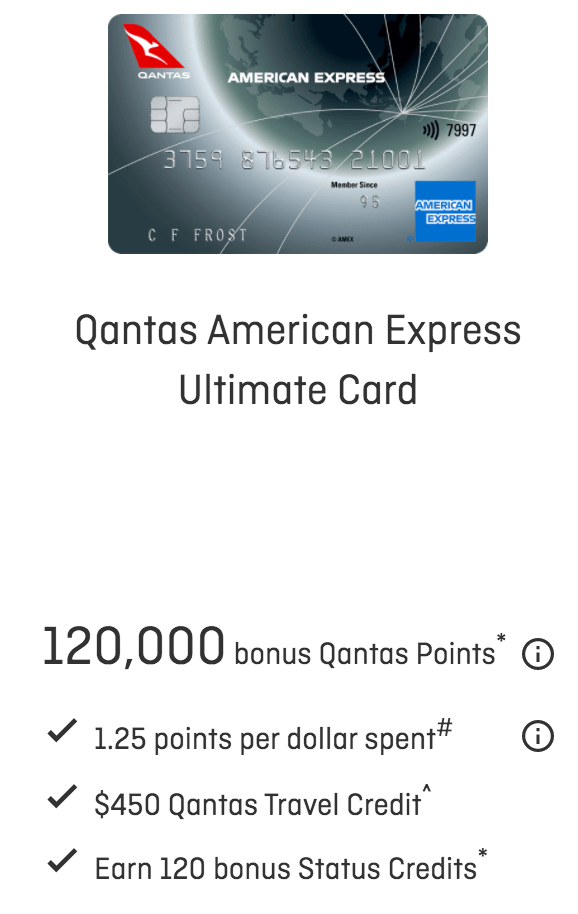

The Qantas American Express Ultimate card is the best Qantas points earning credit card on the market, and right now is the best time to apply for one.

Qantas/AMEX is offering a massive 120,000 points and 120 Status Credits on new cards approved by June 15th 2021.

Even if you used those points for Woolworths vouchers at the worst conversion rate (about half a cent per point), you’d have $600 worth of groceries, more than offsetting the $450 annual card fee. And you’d still have $450 to splurge on Qantas flights.

Personally I look for redemptions worth at least 2 cents per point, which values this offer at $2400.

What I love about the QA Ultimate card is that it keeps working hard to reward your loyalty. Regular bonus points offers can you really boost your points balance, and cashback promotions help to further offset the annual fee. Contrast this to most bank Visa and Mastercard offerings where the bonuses run out after the initial sign on (and they wonder why we churn credit cards!).

And thanks to a new REFERRAL incentive from Qantas, a couple could theoretically turbo charge their QFF balance by 290,000 points.

This is much better than the AMEX referral incentive where the referrer gets a swag of points but the new card applicant (Referee) gets LESS points than if they had applied independently.

Here’s how it could work for you…

Spouse A applies successfully for a new Qantas Amex Ultimate card

Spouse A receives card and refers to Spouse B

Spouse B uses referral link to apply for a new Qantas Amex Ultimate Card

Points Earned:

Spouse A New Card: 120,000

Spouse A Referral: 50,000

Spouse B New Card: 120,000

Total points: 290,000

Even if Spouse A is an existing member they could refer to Spouse B and generate 170,000 points. They would then each have $450 annual card fee and $450 Qantas flights credit, OR if not wanting to hold two accounts, Spouse A could close their account and continue as an additional card holder (free) on Spouse B’s account.

To find your referral link, login to your Qantas Frequent Flyer account, go to My Account, and look through My Offers.

If you don’t already have the card, you can apply for one through this link: (full disclosure, this is my link and I’ll receive 50K points and you will benefit from the full current points offer if you apply by 15th June 2021)